Originally Posted by TwistedChief:

Obviously, Vanguard isn�t a bank. So there�s no FDIC protection. But if you have it in the Vanguard money fund, it�s as safe as anything on planet earth. No need to spread it beyond that. Any cash you need for regular outlays keep in your bank but the rest of the cash you want to preserve should go to the Vanguards of the world.

I can understand people being lazy about this in a world of zero rates. Then a bank or a money market fund were all the same thing. But now most banks are still paying maybe 1-2pct (though other banks are trying to attract deposits and paying more) while money funds are paying levels approaching 5pct.

So the 1-2pct option is basically a loan to a bank where the 5pct option is a loan to the government. You receive a much better return on the latter and have significantly less risk (if you want to bring up the debt ceiling, we can discuss, but that�s a longer conversation and doesn�t remotely change this conclusion).

These Silicon Valley idiots were exceptionally lazy and careless in their cash management. And that allowed SVB to operate as it did until it couldn�t.

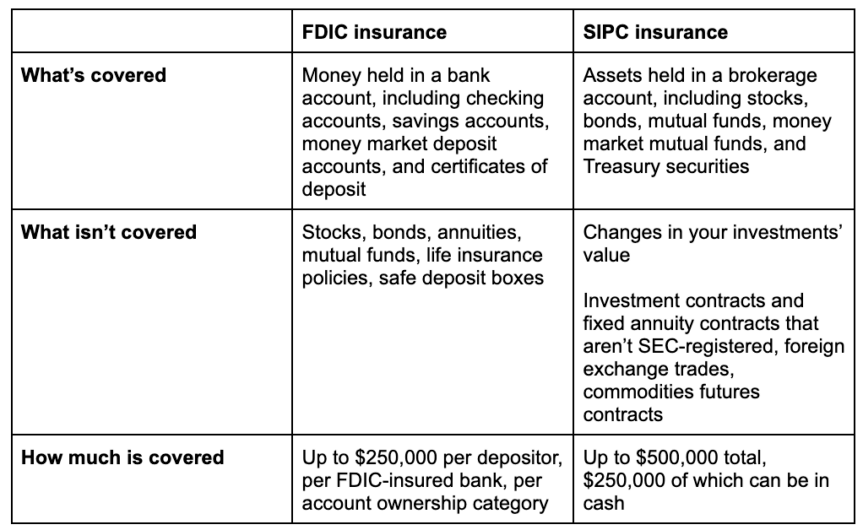

Investments are protected in similar fashion, by SIPC though correct? So just as important to have them spread out as well?

Originally Posted by lewdog:

Investments are protected in similar fashion, by SIPC though correct? So just as important to have them spread out as well?

Thanks for your information.

Nah. Unless Vanguard were taken down due to some massive fraud where your assets were commingled and then stolen in a Madoff-esque fashion, I don�t think you need to spread things out.

Huge institutions invest with money managers all the time - it�s their easiest avenue to deploy capital into the markets - and they definitely aren�t spreading out a $5bn allotment amongst a thousand different managers. [Reply]

Originally Posted by ChiefRocka:

Via infamous bailouts funded with American taxpayer dollars

It's a bailout to provide insurance for a fee? I guess.

Your job that I presume you have right now wouldn't exist if the government hadn't taken those steps. Insured depositors in those same banks wouldn't have been made whole if the government hadn't taken those steps. [Reply]

I assume you are talking about funds like VMRXX, VMFXX, or VUSXX. Is that right or is there something else that you'd recommend parking extra cash in with Vanguard?

And if it is funds like that trio, is there one that you recommend over the other?

I assume you are talking about funds like VMRXX, VMFXX, or VUSXX. Is that right or is there something else that you'd recommend parking extra cash in with Vanguard?

And if it is funds like that trio, is there one that you recommend over the other?

Thanks.

Hey, man - I'm not necessarily recommending anything, but those do a pretty good job of replicating true risk free USD short rates and have risk to nothing aside from the US government.

And yes, those funds.

By virtue of my job I tend to keep more in cash than what anyone would recommend, and 4.5-5% seems delightful relative to some riskier things that I get pitched with IRRs maybe 2x that. [Reply]

In any case, government stepped in to make uninsured depositors in SVB whole. If the government loses money, they essentially tax the banks.

Fed comes out strong providing liquidity to other banks who may experience outflows. Outflows will happen but this is still best case scenario for weaker banks.

I'm sure this story will still percolate and simmer but the tail risks meaningfully reduced in my mind. [Reply]

Originally Posted by TwistedChief:

Hey, man - I'm not necessarily recommending anything, but those do a pretty good job of replicating true risk free USD short rates and have risk to nothing aside from the US government.

And yes, those funds.

By virtue of my job I tend to keep more in cash than what anyone would recommend, and 4.5-5% seems delightful relative to some riskier things that I get pitched with IRRs maybe 2x that.

Thanks, man. I just wanted to make sure I was on the right track (and definitely not holding you to anything if we somehow discover that John Bogle had the biggest pyramid scheme of all time). I've been meaning to shift some cash from my low-interest-bearing account in a credit union for a few months. I already have an account with Vanguard with a total market index fund, so this will be easy. Appreciate you! [Reply]

I've got a big clump of money in one private online broker, which makes me a little nervous. It just kind of happened for various reasons. I keep pondering whether I should move some to another broker just to be sure no catastrophe strikes. Should I? It sounds like I shouldn't be worried that one of the big mainstream brokers will suddenly go belly up.

I would have never used the words "CDs" and "bold" in the same sentence before, but I'm making a bold move into CDs. I've been buying them on 1-5 year time frames with the plan that inflation will go down and I'll end up with CDs that are beating inflation. I think it's a reasonable bet, and my goal is just to match or beat inflation at this point. I think rates are still going up, so I'm buying into them somewhat slowly right now. I'm not putting anywhere near $250k into any one CD, but they're mostly going through the one brokerage, so I hope that's not a risk. [Reply]

Originally Posted by Rain Man:

I've got a big clump of money in one private online broker, which makes me a little nervous. It just kind of happened for various reasons. I keep pondering whether I should move some to another broker just to be sure no catastrophe strikes. Should I? It sounds like I shouldn't be worried that one of the big mainstream brokers will suddenly go belly up.

I would have never used the words "CDs" and "bold" in the same sentence before, but I'm making a bold move into CDs. I've been buying them on 1-5 year time frames with the plan that inflation will go down and I'll end up with CDs that are beating inflation. I think it's a reasonable bet, and my goal is just to match or beat inflation at this point. I think rates are still going up, so I'm buying into them somewhat slowly right now. I'm not putting anywhere near $250k into any one CD, but they're mostly going through the one brokerage, so I hope that's not a risk.

Curious. What rate are you getting on those bank CDs? And how does that compare with US Treasury yields? [Reply]

Originally Posted by TwistedChief:

Curious. What rate are you getting on those bank CDs? And how does that compare with US Treasury yields?

I started doing my CD laddering at around 4.8 percent. The last one I bought was 5.4 percent for a 2-year CD. I'm not famiilar with the banks offering them, but the brokerage is saying that they're FDIC-insured. See the first photo below toward the right side. This is a search that I just did for 2-year CDs.

I keep looking at Treasuries, but I don't know enough about them. The second photo is what I see when I do a search. I used 2-year Treasuries to be consistent across both pictures.

I don't understand what the variables are. I tried looking them up, and the key to me seemed like the "Yield to Worst", which was explained as the worst-case scenario yield. But that implies that there are situations where I can do better than that. And the Coupon seems important because I read that that's the nominal rate, but they're all over the board and I don't know what that means. Why would I be expecting a 4.679+ return off of a bond that has a 1.125 percent nominal rate? I'm sure I'm misunderstanding something.

What I see is that the CD rates are higher and I understand them, so that's what I've been buying. Can you explain why Treasuries should be considered when looking at the two pictures below? Thanks in advance.

Here's something I find kind of humorous. I saw that 5-year CDs were being offered up to 5.4 percent, so I looked at them. The top offerer is the "Bank of Bird-in-Hand".

Does that sound scammy or what? So I looked up this bank, and it turns out that it's a small bank that's located in the town of Bird-In-Hand, Pennsylvania. It caters mostly to Amish people, and in fact their drive-through window is designed to accommodate horses and buggies.

I might have to put a little money into this Amish bank's 5.4 percent rate.

Originally Posted by Jenson71:

I would go with that bank. After all, it's better to have an account with Bank of Bird-in-Hand than two at Bank of Bird-in-Bush.

The Bank of Bird-In-Bush seems too good to be true. I'm wary.

I wonder if the Bank of Bird-In-Hand will give me my monthly dividend in $20 gold pieces. Because that would be kind of cool. [Reply]

{kind=link}