Originally Posted by TwistedChief:

Of course you should. Absolutely. Though if you choose to do it, you�re likely safer with a Chase, Citi, or BOA.

And guys, re: the 1.3%. You do realize that during the largest financial crisis of our lives no depositors whether insured or uninsured lost money, right? Despite several hundred bank failures? There are assets against these bank deposits. And banks are so much more heavily regulated now than they had been (though a former unnamed president watered down regulations for smaller banks).

This SVB situation is super niche. They just did every stupid thing you could�ve done given their structure. Total mismanagement.

Okay, now what am I going to do with this cave and ammunition that I just bought? I can eat the pallets of canned goods, so that's not a problem. [Reply]

Originally Posted by TwistedChief:

Just to take it a step further:

They have about 165bn of deposits. They also have 15bn of Federal Home Loan Bank liabilities that are collateralized and senior to those deposits. Total liabilities = 180bn.

On the asset side they have have 75bn-ish of liquid securities like Treasuries, mortgage-backed securities, etc. They have 40bn-ish of cash. And then they have 75bn-ish of loans which are the murkier part and you�d have to assume a larger discount if someone were to take them off your books immediately� So let�s say 15% which gets you to 65bn..

Assets =180bn

Liabilities = 180bn (75+40+65)

This isn�t to say this analysis is foolproof and everyone will absolutely get fully paid out. But 1/ I bet there will be a solution found where ultimately everyone will get paid out; 2/ no one lost their entire savings; 3/ in bank restructurings in the past pre-financial crisis even 80% recovery on uninsured deposits was really low; 4/ if things don�t get fully solved beyond this weekend, I imagine there will be a bridge solution where uninsured depositors receive something like 50% of their money immediately and then more over time as the assets are disposed of.

The world won�t end.

Yep. The issue here isn't everyone losing their money. The issue is that a ton of businesses temporarily lost access to capital, and it may take a little time for them to get it back. [Reply]

Originally Posted by TwistedChief:

Of course you should. Absolutely. Though if you choose to do it, you�re likely safer with a Chase, Citi, or BOA.

And guys, re: the 1.3%. You do realize that during the largest financial crisis of our lives no depositors whether insured or uninsured lost money, right? Despite several hundred bank failures? There are assets against these bank deposits. And banks are so much more heavily regulated now than they had been (though a former unnamed president watered down regulations for smaller banks).

This SVB situation is super niche. They just did every stupid thing you could�ve done given their structure. Total mismanagement.

I�ve actually kind of done this over the past few years anyway without really thinking about it. I�ve had people tell me, just put it all together so it�s easy to track! Bitch, that�s what spreadsheets are for!

I have our investments spread between Vanguard, T Rowe Price and TD Ameritrade. Our liquid cash is between US Bank and Chase.

Originally Posted by lewdog:

I’ve actually kind of done this over the past few years anyway without really thinking about it. I’ve had people tell me, just put it all together so it’s easy to track! Bitch, that’s what spreadsheets are for!

I have our investments spread between Vanguard, T Rowe Price and TD Ameritrade. Our liquid cash is between US Bank and Chase.

Thanks for your info on this.

Obviously, Vanguard isn’t a bank. So there’s no FDIC protection. But if you have it in the Vanguard money fund, it’s as safe as anything on planet earth. No need to spread it beyond that. Any cash you need for regular outlays keep in your bank but the rest of the cash you want to preserve should go to the Vanguards of the world.

I can understand people being lazy about this in a world of zero rates. Then a bank or a money market fund were all the same thing. But now most banks are still paying maybe 1-2pct (though other banks are trying to attract deposits and paying more) while money funds are paying levels approaching 5pct.

So the 1-2pct option is basically a loan to a bank where the 5pct option is a loan to the government. You receive a much better return on the latter and have significantly less risk (if you want to bring up the debt ceiling, we can discuss, but that’s a longer conversation and doesn’t remotely change this conclusion).

These Silicon Valley idiots were exceptionally lazy and careless in their cash management. And that allowed SVB to operate as it did until it couldn’t. [Reply]

ThaVirus 03-11-2023, 10:05 PM

This message has been deleted by ThaVirus.

Reason: Wrong thread lol

Originally Posted by TwistedChief:

And guys, re: the 1.3%. You do realize that during the largest financial crisis of our lives no depositors whether insured or uninsured lost money, right? Despite several hundred bank failures?

.

Can you elaborate on how that was made possible? [Reply]

Originally Posted by TwistedChief:

Of course you should. Absolutely. Though if you choose to do it, you’re likely safer with a Chase, Citi, or BOA.

And guys, re: the 1.3%. You do realize that during the largest financial crisis of our lives no depositors whether insured or uninsured lost money, right? Despite several hundred bank failures? There are assets against these bank deposits. And banks are so much more heavily regulated now than they had been (though a former unnamed president watered down regulations for smaller banks).

This SVB situation is super niche. They just did every stupid thing you could’ve done given their structure. Total mismanagement.

Originally Posted by TwistedChief:

Obviously, Vanguard isn�t a bank. So there�s no FDIC protection. But if you have it in the Vanguard money fund, it�s as safe as anything on planet earth. No need to spread it beyond that. Any cash you need for regular outlays keep in your bank but the rest of the cash you want to preserve should go to the Vanguards of the world.

I can understand people being lazy about this in a world of zero rates. Then a bank or a money market fund were all the same thing. But now most banks are still paying maybe 1-2pct (though other banks are trying to attract deposits and paying more) while money funds are paying levels approaching 5pct.

So the 1-2pct option is basically a loan to a bank where the 5pct option is a loan to the government. You receive a much better return on the latter and have significantly less risk (if you want to bring up the debt ceiling, we can discuss, but that�s a longer conversation and doesn�t remotely change this conclusion).

These Silicon Valley idiots were exceptionally lazy and careless in their cash management. And that allowed SVB to operate as it did until it couldn�t.

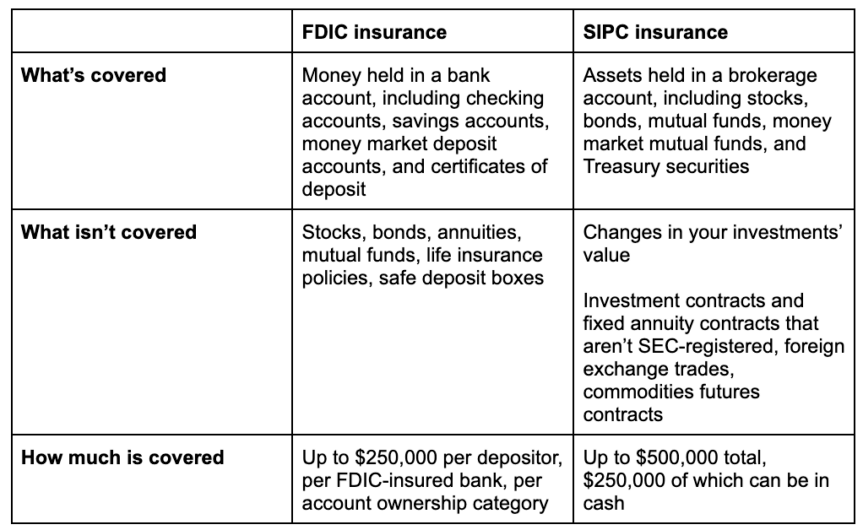

Investments are protected in similar fashion, by SIPC though correct? So just as important to have them spread out as well?

Originally Posted by lewdog:

Investments are protected in similar fashion, by SIPC though correct? So just as important to have them spread out as well?

Thanks for your information.

Nah. Unless Vanguard were taken down due to some massive fraud where your assets were commingled and then stolen in a Madoff-esque fashion, I don�t think you need to spread things out.

Huge institutions invest with money managers all the time - it�s their easiest avenue to deploy capital into the markets - and they definitely aren�t spreading out a $5bn allotment amongst a thousand different managers. [Reply]

Originally Posted by ChiefRocka:

Via infamous bailouts funded with American taxpayer dollars

It's a bailout to provide insurance for a fee? I guess.

Your job that I presume you have right now wouldn't exist if the government hadn't taken those steps. Insured depositors in those same banks wouldn't have been made whole if the government hadn't taken those steps. [Reply]

I assume you are talking about funds like VMRXX, VMFXX, or VUSXX. Is that right or is there something else that you'd recommend parking extra cash in with Vanguard?

And if it is funds like that trio, is there one that you recommend over the other?

I assume you are talking about funds like VMRXX, VMFXX, or VUSXX. Is that right or is there something else that you'd recommend parking extra cash in with Vanguard?

And if it is funds like that trio, is there one that you recommend over the other?

Thanks.

Hey, man - I'm not necessarily recommending anything, but those do a pretty good job of replicating true risk free USD short rates and have risk to nothing aside from the US government.

And yes, those funds.

By virtue of my job I tend to keep more in cash than what anyone would recommend, and 4.5-5% seems delightful relative to some riskier things that I get pitched with IRRs maybe 2x that. [Reply]

In any case, government stepped in to make uninsured depositors in SVB whole. If the government loses money, they essentially tax the banks.

Fed comes out strong providing liquidity to other banks who may experience outflows. Outflows will happen but this is still best case scenario for weaker banks.

I'm sure this story will still percolate and simmer but the tail risks meaningfully reduced in my mind. [Reply]

{kind=link}